Germany: The Relentless Reign of Cash

Walk into a bakery in Berlin, and you might be surprised to see a “Cash Only” sign still hanging by the register. Despite being a powerhouse in the European Union, Germany clings to cash with a tenacity that baffles many outsiders. According to a 2024 Deutsche Bundesbank report, about 60% of all transactions in Germany are completed with physical money. This is not just habit—it’s a deep-seated cultural attitude shaped by decades of skepticism toward debt and surveillance. Many Germans feel that cash offers privacy and control over spending, acting almost like a personal budgeting tool. ATMs are on nearly every corner, and most shops, even in trendy neighborhoods, won’t blink if you hand over banknotes instead of plastic. There’s also a lingering unease about credit cards stemming from concerns over data collection. As a result, even as digital wallets and contactless payments become popular among younger people, the majority still prefer the familiar comfort of cash.

Japan: A Cautious Approach to Borrowed Money

Japan’s glossy cities and technological prowess might suggest a nation obsessed with the latest in financial gadgets, but the reality on the ground tells a different story. As of 2025, only about 30% of Japanese people use credit cards regularly, according to the Japan Consumer Financial Behavior Study. The reason lies in the country’s cultural emphasis on saving and avoiding debt at all costs. Many Japanese folks view credit cards with suspicion, equating them with overspending and financial instability. Instead, they gravitate toward debit cards and cold, hard yen. The popularity of prepaid IC cards like Suica and Pasmo for everything from train rides to shopping only underlines this cautious mindset. Family traditions, often passed down through generations, reinforce the idea that borrowing—even just for a month—should be the exception, not the rule. Even tech-savvy youth tend to stick with mobile payments and cash, keeping credit cards on the sidelines.

Sweden: Mobile Payments Lead the Way

Mention Sweden and “cashless society” often springs to mind, but the Swedish story is more nuanced. While only about 20% of transactions are now done with cash, credit card usage also remains moderate, with roughly 40% of Swedes using them regularly, according to the 2024 Swedish Payment Trends Report. The reason is the spectacular rise of Swish, a mobile payment app that has become almost ubiquitous. Swish allows instant money transfers via smartphone, and it’s used everywhere—from flea markets to charity donations. In this tech-forward nation, convenience rules, and Swish’s seamless user experience has made it the go-to choice for millions. Even small businesses and street vendors prefer Swish payments over credit cards, which often come with higher fees and slower processing. This collective leap into mobile payments has made credit cards feel almost old-fashioned, despite Sweden’s reputation for embracing modernity.

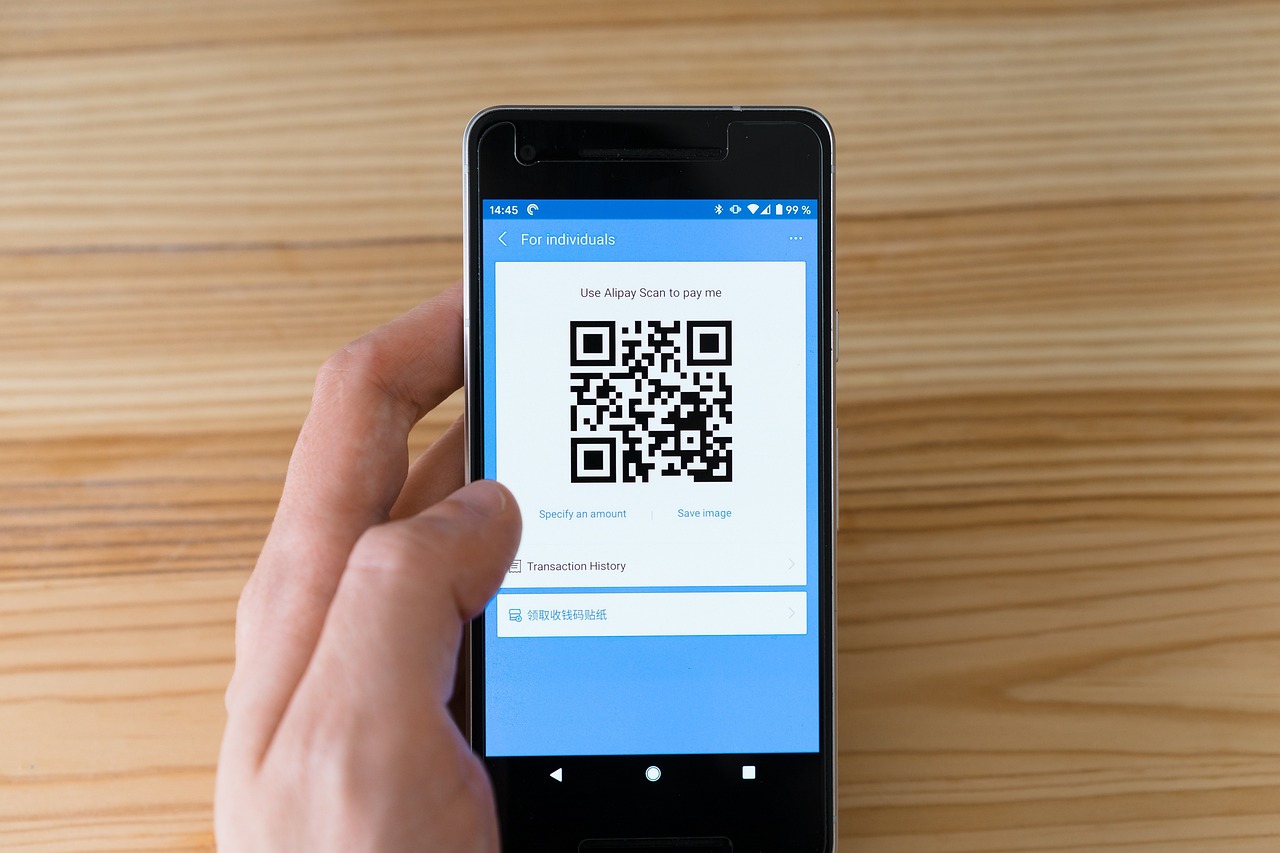

China: Digital Wallets Take Center Stage

China’s transformation in payment habits has been nothing short of astonishing. Forget about credit cards—2023 data shows only 15% of transactions nationwide happened on credit cards, according to China Digital Payment Statistics. The stars of the show are Alipay and WeChat Pay, digital wallets that have become integral to daily life. From street food vendors to luxury malls, QR codes rule the marketplace. The sheer convenience of paying with a smartphone has made plastic cards seem clunky and outdated, especially among younger generations. The Chinese government has also encouraged cashless transactions to streamline the economy, which has only accelerated the trend. Even older citizens are adapting, using digital payments for everything from groceries to medical bills. Credit cards, with their higher barriers to approval and limited rewards, can’t compete with the speed, ease, and perks of mobile wallets.

India: Cash Still Wears the Crown

India’s streets buzz with life, and so do its cash transactions. Despite government pushes toward digital payments, cash still accounts for about 70% of all transactions as of 2024, as reported in the Indian Financial Inclusion Report. Credit card usage remains very low, with only around 5% of the population regularly swiping cards. Deep-rooted traditions, a large unbanked population, and the patchy reach of formal banking mean that cash is the safest bet for millions. Even with the rise of UPI (Unified Payments Interface) and mobile wallets like Paytm, people tend to use digital means for small, daily purchases rather than major spending. Trust in cash is so ingrained that it’s common to see wedding gifts and big purchases paid in cash bundles. While India’s digital payment revolution is real and growing, especially in cities, credit cards are still outpaced by both cash and newer, easier-to-access mobile solutions.

Italy: Tradition and Skepticism Shape Spending

Italy, the land of la dolce vita, isn’t rushing to embrace credit cards either. According to payment industry data from late 2024, only about 30% of Italians regularly use credit cards, with most preferring cash or debit cards for everyday expenses. There’s a strong tradition of cash payments, especially in smaller towns and family-run businesses, where tax transparency is a sensitive issue. Many Italians also feel more secure using cash, concerned about fraud and hidden fees associated with credit cards. The banking system’s complexity and relatively high credit card interest rates add to the public’s reluctance. While contactless and mobile payments are growing, particularly among younger Italians, the cultural preference for cash remains a powerful force. Even in bustling markets and chic boutiques, paying in cash is often expected and welcome.

United Arab Emirates: The Power of Direct Payments

In the United Arab Emirates, one of the world’s wealthiest and most technologically advanced regions, credit card usage remains surprisingly low compared to other financial hubs. 2024 data indicates that less than 35% of residents use credit cards as their primary payment method. The reason is the prevalence of direct bank transfers, debit cards, and local payment apps that dominate everything from shopping to bill payments. Many residents, particularly expatriates, favor prepaid and debit cards, which are simpler to obtain and use without incurring debt. There’s also a strong governmental push for secure, traceable transactions, which has led to a preference for payment methods linked directly to bank accounts. Cultural attitudes also play a role, as many people in the UAE prefer to spend only what they have, avoiding the risk of interest and debt. Even as luxury shopping and high-end tourism thrive, the humble debit card and mobile wallet often win out over the flashier credit card.